The Deal Everyone Won (And No One Did)

This was the rare war where everyone won—and that is precisely the problem.

This is a scenario—a thought exercise. Not a prediction, but a structured way to think about how power, perception, and markets may evolve when all sides claim victory and no side truly loses.

It begins, as these things now do, on television. Donald Trump appears live—grinning, expansive, claiming total victory. In one pocket, metaphorically, sits Nicolás Maduro; in the other, the Ayatollah. The moment is surreal, theatrical, and entirely on brand. Fox News celebrates while CNN laments. Gas drops to $2 a gallon, and the GOP declares victory.

And, almost unbelievably, so does Iran.

In Tehran, the streets fill. The Ayatollah declares triumph—not just survival, but transformation. The Islamic Republic, he claims, has evolved into something more durable: a theocratic–hereditary order, stabilized under pressure and legitimized through endurance. Iran did not win on the battlefield; it won by not losing. In modern conflict, that is often enough.

Behind the spectacle lies the real story. A deal—never fully written and never formally acknowledged—has been made. Not a peace, but a redistribution of influence dressed up as victory.

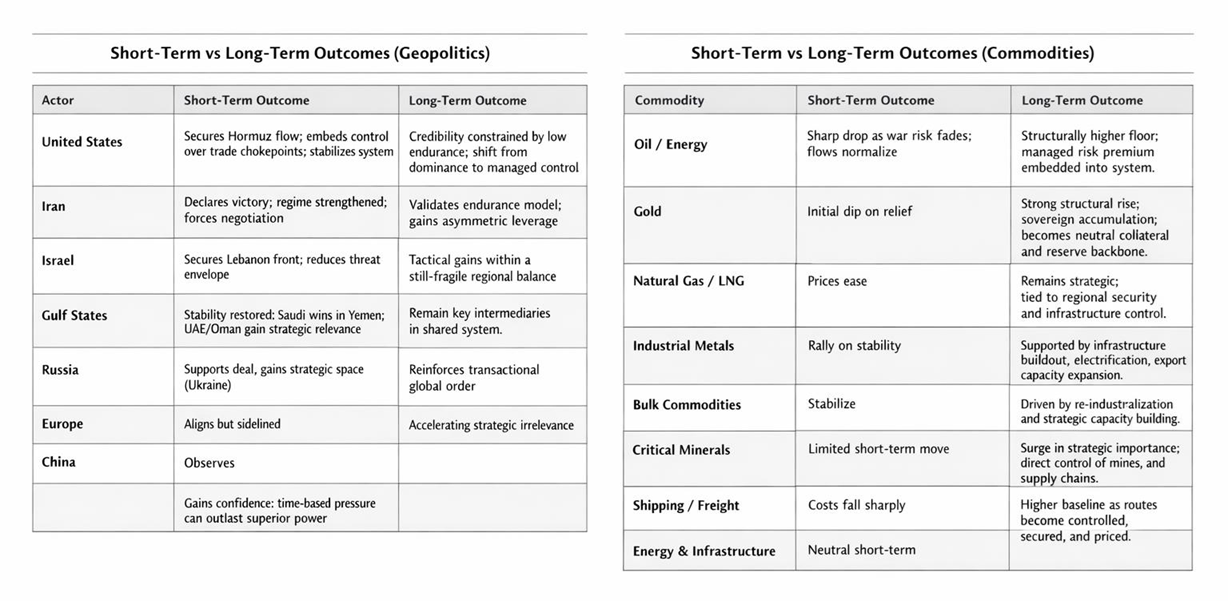

Yemen is quietly settled. Saudi Arabia secures its core interests and exits with a long-delayed win. Lebanon tilts decisively into Israel’s strategic envelope, allowing Benjamin Netanyahu to claim success—no nuclear threat and a northern front effectively contained. Pakistan’s General Asim Munir also declares victory, as such outcomes tend to allow.

At the center sits the real arrangement. The Strait of Hormuz is no longer a battlefield but a managed system. Oman and the UAE act as intermediaries, Iran remains inside the framework, and the United States anchors the structure without fully owning it. It is stability without full control—a system held together rather than resolved.

Shipping flows resume and energy stabilizes. In the short term, escalation is contained, chokepoints function, and allies are reassured. The United States secures the flow through Hormuz and embeds itself deeper into the control of global trade routes.

But the deeper shift is more consequential. This was never just about Iran—it was about flow. With influence over Hormuz and continued dominance over Panama, the United States sits astride the arteries of global trade. Security becomes a service, stability becomes a product, and access is quietly priced. The system is not merely protected; it is monetized.

Power shifts from owning resources to controlling the routes through which they move. What emerges is not isolationism, but a doctrine of pathways. At a deeper level, this can be understood as an attempt to contain China—not through direct confrontation, but through control of the system China depends on.

In Ender’s Game, Earth pushes the enemy back and contains it within a bounded space. But reality is not fiction. China is not static; it has already demonstrated the capacity to absorb pressure, adapt, and plan across long horizons. Containment is not closure—it is positioning.

The United States may shape the system today, only to encounter the same challenge again under different timelines and conditions. America may have the watch, but China may have the time.

Yet this cuts both ways. China learns that endurance can force outcomes, but also that miscalculation at scale carries systemic risk. The lesson is not simply confidence; it is calibration.

Markets, too, celebrate. Oil prices fall sharply as war risk fades and flows normalize. Risk premia collapse and shipping stabilizes. For a moment, it appears as if the system has reset—energy is cheap, volatility subsides, and stability returns.

But only for a moment.

Because this was not a resolution. The system did not break; it revealed its terms.

Oil no longer trades purely on scarcity; it acquires a structural floor shaped by geopolitics and controlled routes. What replaces the war premium is a managed risk premium embedded in the system itself. Natural gas and LNG markets ease in the short term, but remain strategically tied to regional security frameworks and infrastructure control.

Gold tells the deeper story. It dips initially as immediate fear subsides, but then rises again—steadily and structurally. This rise is not driven by panic, but by policy. States begin to accumulate gold as a neutral reserve asset, a form of collateral that sits outside geopolitical alignment. It becomes, in effect, the balance sheet behind sovereignty.

Industrial metals such as copper and aluminum rally in the short term on renewed stability, but their longer-term trajectory is driven by infrastructure buildout, electrification, and the expansion of export capacity. Bulk commodities like iron ore and steel stabilize initially, but are increasingly tied to re-industrialization and strategic capacity building.

Critical minerals—lithium, rare earths—show limited immediate movement, but their long-term importance surges as nations seek direct control over mines and supply chains. Shipping and freight costs fall sharply in the short term, yet settle at a higher structural baseline as routes become controlled, secured, and priced. Energy and resource infrastructure, relatively unchanged in the immediate aftermath, emerges as a premium asset class, with states investing heavily in ports, pipelines, refining, and defense-linked production.

Across the world, nations draw the same conclusion: the U.S. security umbrella is no longer absolute. What follows is not fragmentation, but self-insurance at scale. States build reserves—not just of oil, but across commodities. They secure supply chains, acquire resource assets, and invest in logistical control.

Commodities are no longer simply traded. They are secured.

A more critical view—contested, but increasingly voiced—suggests that Europe is attempting to sustain a conflict without matching financial, military, or energy depth. Having reduced reliance on Russian energy, it finds itself more dependent on external supply and U.S. guarantees. It is not irrelevant, but it is increasingly reactive rather than decisive—present in cost, yet peripheral in outcome.

Russia, in this view, benefits not through decisive victory, but through shaping the field—stretching timelines, shifting priorities, and creating space in Ukraine. It is not a clean win, but it is a repositioning that reinforces a more transactional global order.

China observes. It does not rush forward; instead, it recalibrates. The lesson is not simply that power can be challenged, but that time can be used as an instrument of strategy. Pressure, applied patiently, can reshape outcomes.

On the surface, this still appears to be order. The United States stabilizes the system, Iran legitimizes itself, Israel secures its front, Gulf states regain stability, and markets recover.

Everyone wins.

And then come the quieter gains. Oman, long seen as a secondary energy player, emerges as a structural beneficiary—its position along Hormuz transforming it into a toll collector of stability, with relevance tied directly to global energy flows. Benjamin Netanyahu is recast from embattled to consequential, strengthening his legacy through territorial and strategic consolidation. General Asim Munir consolidates authority in the short term, strengthening his position within Pakistan’s power structure.

Russia, under Vladimir Putin, secures both immediate and longer-term gains through repositioning. Iran’s regime achieves a short-term victory through survival, while the country itself gains longer-term leverage. Donald Trump’s gains may be more historical—shaping narrative and legacy beyond the immediate moment. Xi Jinping, while tactically restrained in the short term, accrues longer-term strategic advantage through lessons absorbed and time preserved.

Others fare less well. Europe faces erosion in both the short and long term, its role constrained despite its stakes. Ukraine and Volodymyr Zelensky bear losses across both horizons. Turkey, under Erdogan, similarly finds itself weakened in both the immediate and longer-term balance. India’s trajectory under Modi remains less clear—positioned within the system, but not yet fully defined by it.

Almost everyone walks away with something.

Which is precisely the point.

Because the balance of wins masks the shift beneath.

This is not the end of American power, but a change in how—and how long—it is willing to be used. The United States can still control outcomes in the present, but it is increasingly selective in how it expends time, loss, and attention.

Power is no longer defined by control of territory alone. It is defined by endurance—and by control of the routes through which the world moves.

The United States sits atop the system, but it has revealed its thresholds. Adversaries do not need to defeat it; they need to understand it—and wait.

This is not collapse. It is rebalancing—quiet, uneven, and already underway. A world where dominance matters less and resilience matters more; where globalization continues but becomes gated; where commodities are secured, not just priced; and where routes matter as much as resources.

This is not resolution.

It is transition.

America controls the system. Its rivals, increasingly, control time.

This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.