India’s Market Is Warning About Lower Growth

The market is pricing a tougher future. Policy must deliver a stronger one.

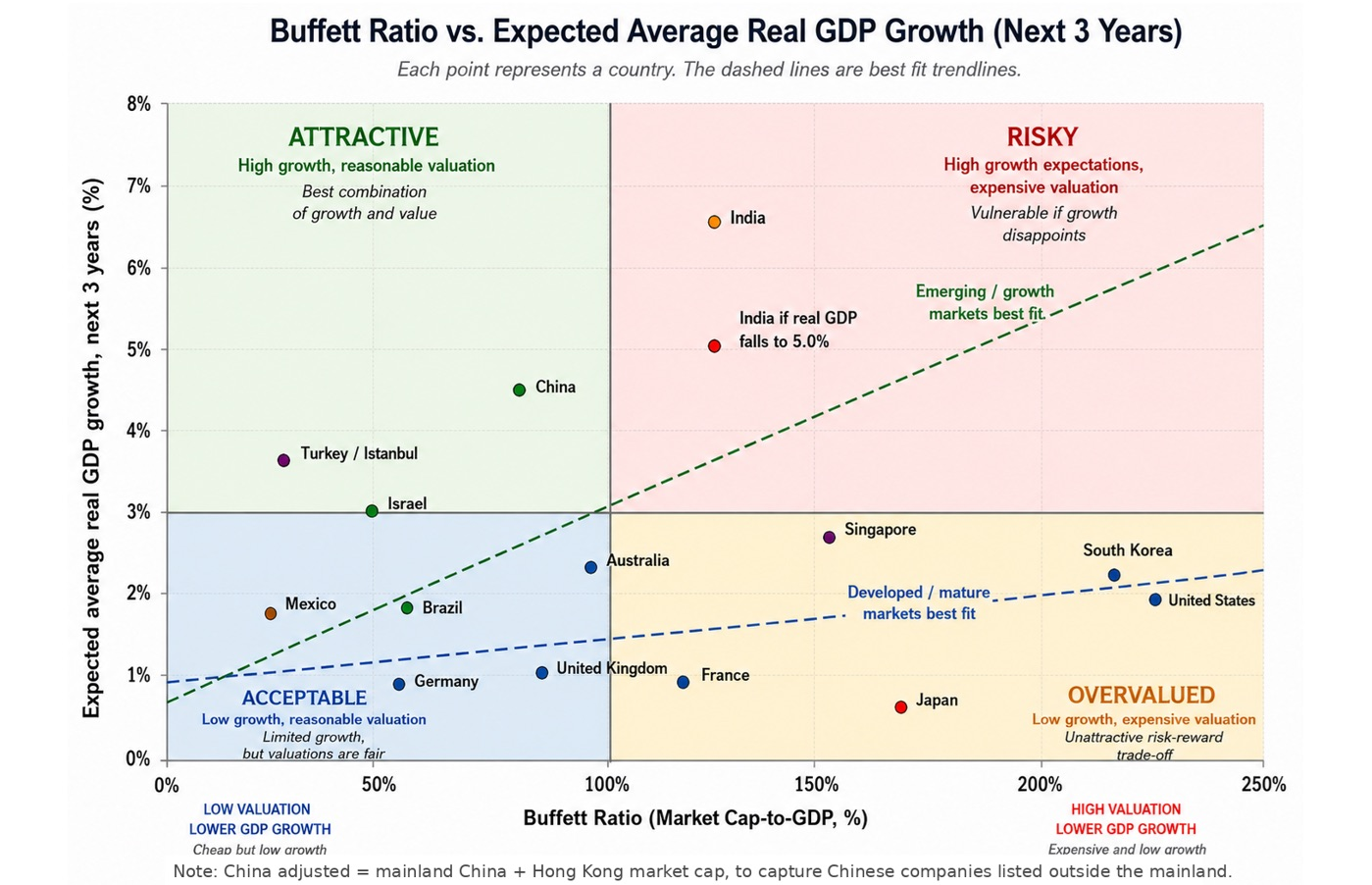

At current levels, India’s stock market is no longer pricing a cheap growth story. It is pricing a more difficult reality: India may be at risk of becoming a lower-growth economy.

The market is not saying India will grow at 7–8% real GDP forever. It appears to be pricing something closer to a 5–6% real growth economy — still respectable, but no longer exceptional enough to justify complacency.

That is the warning.

Note: China adjusted = mainland China + Hong Kong market cap, to capture Chinese companies listed outside the mainland.

India cannot afford to let its growth premium erode. If the government wants to protect that premium, it has to loosen the constraints on growth. That means reducing fiscal wastage, improving the quality of public spending, accelerating infrastructure execution, lowering friction for private investment, easing the burden on businesses, and allowing more capital to flow into productive sectors.

India does not need more headline spending. It needs better spending.

The risk is that too much fiscal capacity is absorbed by subsidies, bureaucracy, leakage, and low-return expenditure, while too little goes into productivity, logistics, manufacturing depth, energy security, and private-sector confidence. If that continues, India’s growth ceiling will fall.

And the market is already beginning to price that risk.

The market is giving India a warning, not a guarantee.