Butter Chicken Doesn’t Help Lose Weight : Vikas Sehgal

Vasuki Perspectives · Notes on Money & Motive Butter Chicken Doesn’t Help Lose Weight by Vikas Sehgal The other evening, I had dinner near Mumbai airport before catching my flight home. Whenever I am in Mumbai, I make sure I see him for dinner — and he has a remarkable habit of asking questions that stay with me long after the meal is over. This essay is the result of one of those questions. As a good Punjabi, I was enthusiastically demolishing butter chicken with naan. As a good Gujarati observing Ekadashi, he was perfectly content with fruit and a cold coffee. I happen to be on a determined mission to lose weight. He, rather annoyingly, has already succeeded. That evening, two things wanted to happen. I wanted to lose weight. India wanted more foreign investment. Neither, I suspected, was going to happen without changing course in a dramatic way. As I reached for another piece of naan, our conversation drifted to the Federal Reserve, the rupee and the surprisingly modest flow of foreign portfolio investment into India. Somewhere between the butter chicken and his fruit plate, it struck me that my dinner and India’s investment policy suffered from exactly the same problem. Both had admirable intentions. Neither had aligned its actions with those intentions. Businesses create wealth. Policy determines how much of that wealth survives the journey back to its owners. Where did the ₹20 go? Illustrative economic journey, ₹100 invested Value Initial investment ₹100 Value after one year ₹120 Less: corporate tax −₹5 Less: dividend tax −₹6 Less: INR vs USD (illus.) −₹5 Less: USD vs gold (illus.) −₹8 Real value retained ₹96 Not an accounting statement — an illustration of how successive policy leakages erode the real value a foreign investor ultimately retains. Same ₹100, different choices Route After 1 yr Indian company ₹96 GoI security (6%) ₹106 USD FCNR deposit (6%) US$106 The state seeks foreign capital for enterprise while offering sovereign alternatives that compete for the same capital — financing itself with the very flows it says it wants private business to receive. “Capital has no passport, no ideology and no sentiment. It simply follows incentives.” The irony is that the Indian state both seeks foreign capital for enterprise and offers attractive sovereign alternatives that compete for the same capital. In effect, it is consuming the very foreign capital it says it wants private enterprise to receive, while incentivising investors to finance the sovereign instead. As I drove alone to the airport after dinner, I found myself smiling. Judging by the amount of butter chicken and naan I had just consumed, my prospects of losing weight had not improved in the slightest. Wanting to lose weight is not a diet. Wanting foreign investment is not an investment policy. Intentions define the destination. Actions determine whether we ever arrive. Life has a peculiar way of rewarding what we do, not what we wish for. Neither markets nor waistlines negotiate with good intentions. They respond to incentives, discipline and consistent action. Unfortunately, butter chicken and naan have never been part of a successful weight-loss strategy. Perhaps investment policy isn’t very different. VASUKI FUNDS Vasukixvi@vasukiindia.Com Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

The Arithmetic of Wealth : Vikas Sehgal

The Arithmetic of Wealth · Vasuki Perspectives VASUKI PERSPECTIVES FINANCE · WEALTH PRESERVATION The Arithmetic of Wealth The Journey of ₹100: Where Wealth Disappears By Vikas Sehgal Imagine two investors, each beginning with exactly ₹100. Both are intelligent. Both are disciplined. Both select excellent businesses. Twenty years later, one has preserved significantly more purchasing power than the other. The difference was not the stock they selected. The difference was the journey that the ₹100 took before it finally reached them. This framework is intentionally simplified. It is not an accounting exercise or a tax guide, nor is it intended to predict investment returns in different markets. Its purpose is to illustrate a broader economic principle: the cumulative effect of layers of value extraction on long-term investor wealth. Every economy imposes friction on capital through taxation, regulation, compliance costs, transaction costs, inflation and currency movements. Individually, each layer appears manageable. Collectively, they determine how much purchasing power ultimately belongs to the investor. The question therefore is not simply, “How much did my investment earn?” The more important question is: “After every layer of value extraction has taken its share, how much of my original purchasing power remains?” Journey of ₹100 India US UK Singapore Dubai Initial investment 100 100 100 100 100 After remittance costs 100 98 98 98 98 After corporate taxes & institutional costs 60 72 70 74 80 After investor-level taxes 26 40 38 42 48 ₹100 remaining after all frictions 18 32 30 28 35 *Illustrative values intended to demonstrate cumulative structural friction rather than statutory tax calculations. The table is not intended to compare expected market performance. Rather, it illustrates a simple but frequently overlooked reality: an investor never owns only the underlying business. The investor also owns the legal framework, the tax regime, the currency, the regulatory environment and the institutional incentives embedded within the jurisdiction where that capital resides. This explains why the relevant question is not simply, “Which stock will produce the highest return?” A more important question is, “How much of that return will ultimately remain in my hands after every layer of value extraction has taken its share?” Perhaps this also explains one of India’s oldest investment habits. For generations, Indian households quietly accumulated gold instead of financial assets. Whether by instinct or experience, they understood a timeless principle: the fewer intermediaries standing between you and your wealth, the fewer opportunities there are for value to be extracted before it reaches you. Investors spend enormous effort selecting the right company. They analyze management quality, competitive positioning, earnings growth and valuation. Far fewer spend equal time studying the economic system through which those returns must travel before the wealth finally reaches them. Yet, over decades, the system can matter as much as the investment itself. Stock selection determines relative performance within a market. The choice of jurisdiction determines the structural environment within which every investment compounds. A great company can outperform its peers. A great system allows that outperformance to reach the shareholder. For the global investor, therefore, the first question is not: “Which company should I own?” It is: “Which system should my capital live in?” Every investor begins with the same ₹100. The difference is not where the journey starts. The difference is how much of that ₹100 is still yours when the journey ends. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

My Mother’s Pressure Cooker : Vikas Sehgal

My Mother’s Pressure Cooker · Vasuki Perspectives VASUKI PERSPECTIVES CURRENCY · FISCAL POLICY My Mother’s Pressure Cooker Why the Rupee May Be India’s Fiscal Safety Valve By Vikas Sehgal When I was a child, I was terrified of my mother’s pressure cooker. Every time it let out a loud whistle, I instinctively thought it was about to explode. Years later, I learnt that the whistle meant exactly the opposite. It wasn’t a warning of failure—it was the mechanism that prevented one. Today, I think about the Indian rupee in much the same way. The debate around the Indian rupee is often framed around exports, imports and capital flows. I believe the more important driver over the coming decade will be fiscal arithmetic. Investors often analyse a currency through the lens of trade balances and interest-rate differentials. I believe they should first analyse the sovereign balance sheet and the political incentives that shape it. India has accumulated a large stock of rupee-denominated obligations through subsidies, free food programmes, welfare schemes such as Ladli Behna, pensions and other social commitments. As these commitments become politically difficult to reverse, they increasingly resemble long-duration liabilities on the sovereign balance sheet. These promises are liabilities in the state’s own currency. History suggests that governments with liabilities denominated primarily in their own currency rarely default outright. Instead, they reduce the real value of those obligations through inflation and gradual currency depreciation. Inflation allows the state to remain politically popular while becoming progressively less liable in real terms. For politicians, this creates a powerful incentive. They can make generous promises, deliver them in nominal terms, and yet gradually reduce their real economic cost through inflation. Investors should think carefully about the long-term implications of this dynamic. I therefore believe it is in the long-term fiscal interest of the Indian state for the rupee to depreciate steadily against the US dollar—and even more rapidly against gold. In a democracy where political incentives increasingly favour expanding welfare commitments, currency depreciation becomes the pressure-release valve that allows those promises to be honoured in nominal terms while reducing their real economic cost over time. The obvious counterargument is that a weaker rupee makes imports more expensive. While this is true in principle, India’s primary external vulnerability is oil. Other imports, such as fertilizers and industrial inputs, are comparatively manageable. More importantly, I believe the medium-term outlook for oil prices is structurally lower as significant new supply from South America enters global markets. If oil trends towards US$50 per barrel, India gains the rare opportunity to allow a weaker currency without importing the same degree of inflation that would normally accompany such depreciation. Ironically, a stronger rupee could make India’s fiscal position more difficult. Currency appreciation increases the real value of the government’s rupee-denominated obligations, making an already large fiscal burden even harder to manage. When one looks beyond the Central Government and includes the liabilities of highly indebted states such as Punjab, West Bengal and Kerala, India’s consolidated public-sector debt is considerably higher than headline figures suggest. The rupee should not be viewed merely as an exchange rate. It is a fiscal adjustment mechanism. Like the whistle on my mother’s pressure cooker, gradual currency depreciation releases pressure that would otherwise continue to build within the sovereign balance sheet. Without that safety valve, the adjustment eventually has to come through painful fiscal reforms, significantly higher taxation, much slower growth, or, in the extreme, a fiscal crisis. For that reason, I expect the rupee to depreciate not only against the US dollar, but even more persistently against gold. Gold measures the long-term erosion of purchasing power; the dollar merely measures the value of one fiat currency against another. Fiscal arithmetic cannot be negotiated—it merely reasserts itself over time. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

Remember the Athenians : Vikas Sehgal

Remember the Athenians Remember the Athenians Great Powers Don’t Forget, Rarely Forgive By Vikas Sehgal Let me begin with a disclaimer. I am not predicting the destruction of Iran. I am not claiming that war is inevitable, nor am I arguing that history repeats itself with mechanical precision. What I am describing is a possibility. More accurately, it is a pattern. A pattern that appears frequently enough throughout history that it deserves consideration, particularly at moments when public attention is focused almost entirely on the immediate present. Imagine yourself standing in the palace complex at Persepolis. Dawn light filters through towering columns adorned with carvings of conquered nations bringing tribute to the Great King. Courtiers move quietly through corridors that serve the largest empire on earth. Before Darius I rises from his bed, before ambassadors arrive from distant provinces and generals report from the empire’s frontiers, a servant whispers a simple phrase into the ruler’s ear: “Master, remember the Athenians.” The reference was to Marathon. To modern readers the phrase may appear trivial, but to Darius it carried immense significance. This was not the ruler of a small kingdom nursing a local grievance. This was the master of an empire stretching from Egypt to India, commanding wealth, manpower, and resources on a scale that the Greek city-states could scarcely comprehend. Yet despite that overwhelming superiority, a small collection of Greeks had humiliated him. The reminder was not merely about revenge. It was about memory. Darius understood something that modern analysts often forget. Great powers can survive defeat. They can survive embarrassment. They can survive tactical setbacks. What they struggle to tolerate is allowing those setbacks to become accepted facts. An unanswered humiliation invites repetition. A setback ignored becomes a precedent. A precedent becomes an invitation for further challenge. Persia remembered Marathon not because it changed the balance of power, but because it challenged the perception of power. Persia returned. The defeat was neither forgotten nor accepted. Years later, Xerxes crossed into Greece with one of the largest military expeditions the ancient world had ever seen. The campaigns that followed would ultimately culminate in one of history’s enduring lessons: powerful states may absorb defeat, but they rarely stop thinking about it. Eventually Athens itself would watch its city burn. History contains countless variations of this story. The names change. The geography changes. The technologies change. Human nature does not. Consider Rome after Cannae. In 216 BC Hannibal inflicted one of the most devastating defeats in military history. Tens of thousands of Roman soldiers died in a single day. Entire aristocratic families disappeared on the battlefield. The Republic lost officers, senators, commanders, and citizens on a scale almost impossible to comprehend. Many contemporary observers believed Rome was finished. Rome reached a different conclusion. Instead of negotiating from weakness, Rome absorbed the lesson. It rebuilt its armies, revised its military doctrine, replaced commanders, and fundamentally altered its strategy. Rome understood something that many modern observers struggle to appreciate: battlefield defeats do not necessarily determine the outcome of wars. The willingness to learn from defeat often matters more than the defeat itself. Years later Rome carried the war into Africa. Hannibal was defeated at Zama. Carthage survived temporarily, but Roman memory endured long after the immediate danger had passed. Roman statesmen increasingly embraced a phrase that would echo through history: Carthago delenda est—Carthage must be destroyed. The phrase was less a military objective than a mindset. Rome no longer viewed Carthage as a competitor to be managed. It viewed Carthage as a problem to be eliminated. Eventually it was. The city was destroyed. Its political independence disappeared. Its empire vanished. Its territory was absorbed into Roman control. Whether or not every legend surrounding the destruction is literally true is beside the point. The strategic reality is undeniable. Rome remembered. Rome returned. Rome finished the problem. The same pattern appears in ancient China. Most people know Qin as the state that unified China under Qin Shi Huang. Fewer appreciate how formidable its opponents were. Among them, Chu stood apart. Chu possessed vast territory, abundant agricultural resources, enormous manpower, and a military establishment capable of challenging any rival in the Warring States era. For long periods, Chu appeared every bit as powerful as Qin. The struggle between Qin and Chu was neither quick nor inevitable. Qin suffered reverses. Campaigns failed. Commanders underestimated their opponent. Yet Qin possessed advantages that were not immediately visible on the battlefield. It possessed administrative discipline, institutional capacity, centralized authority, and a political culture obsessed with learning and adaptation. Rather than accepting setbacks, Qin treated them as information. Larger armies were mobilized. Command structures were revised. Strategies were adjusted. Lessons were incorporated. Qin returned repeatedly until the outcome changed. When the struggle finally ended, Qin unified China while Chu disappeared as an independent state. Once again the lesson was not that great powers never lose. The lesson was that they often learn faster than their rivals. Modern history offers similar examples. Russia’s experience in Chechnya illustrates the same phenomenon. The First Chechen War exposed profound weaknesses within the Russian military. Moscow suffered embarrassment, operational failures, and strategic disappointment. Many observers interpreted the outcome as evidence of permanent Russian decline. Russia interpreted it differently. Russian planners studied what had gone wrong. Military structures were revised. Tactics evolved. Resources were concentrated. Years later Russia returned under dramatically different circumstances. The Second Chechen War produced a very different outcome. Grozny was reduced to ruins. Entire districts became symbols of devastation. Whatever moral judgments one attaches to the conflict, the strategic conclusion remains difficult to dispute. Russia did not accept humiliation. It absorbed the lesson and came back with overwhelming force. The common thread connecting Persia, Rome, Qin, and Russia is not invincibility. None of these powers were invulnerable. None were immune from mistakes. All suffered defeats. All experienced setbacks. The common thread is persistence. This distinction matters because modern observers often confuse tactical outcomes with strategic conclusions. A withdrawal is interpreted as acceptance. Restraint

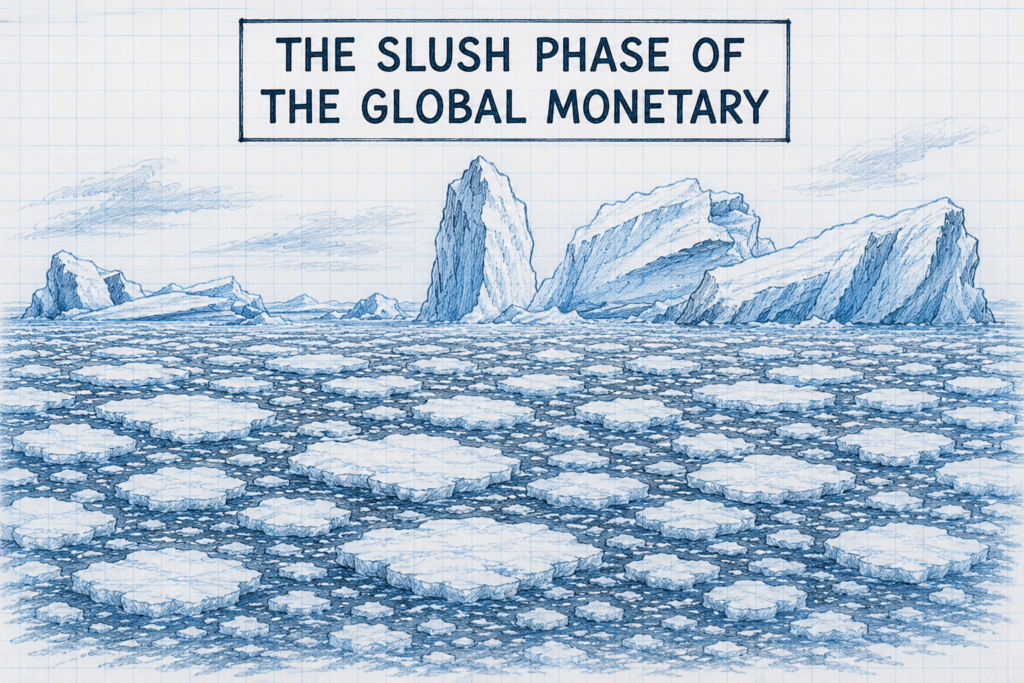

The Slush Phase of the Global Monetary Order : Vikas Sehgal

The Slush Phase of the Global Monetary Order The old system still trades. The new system is already being priced. By Vikas Sehgal When matter changes state, it does not move cleanly from one form to another. Water does not instantly become ice. For a period, it becomes slush — partly liquid, partly solid, carrying the properties of both states. That is where the global monetary system is today. The old dollar-reserve order has not died. But the new order has not fully formed. Markets are stuck between two regimes: the Treasury-centered world of the past and a more fragmented, gold-sensitive, multi-currency world that is beginning to emerge. History shows that monetary systems often outlive the powers that created them. Rome declined, but Roman monetary habits survived for centuries. The denarius lived on in later coinage and language; the word “dinar” descends from it. The dirham, rooted in the older drachma tradition, carried forward another ancient monetary inheritance into the Middle East. A dead empire can still have a living currency. That is the point about the dollar today. Even if the American-led order is weakening, the dollar will not vanish overnight. It remains embedded in trade contracts, central-bank reserves, debt markets, commodity pricing, and institutional memory. The old system can be politically exhausted and still financially alive. Under the old regime, the market reaction to war was simple. Geopolitical stress meant the dollar strengthened, Treasuries rallied, yields fell, and gold rose. The dollar was the refuge. Treasuries were the safe asset. Gold was the insurance policy. Today the signals are no longer clean. Yields can rise even when fear rises. Treasuries can sell off even when geopolitical risk increases. Gold can fall tactically even as its strategic role strengthens. The dollar can weaken without collapsing. That is not irrationality. It is transition. The United States remains the center of the financial system, but it is no longer seen as the neutral custodian of that system. China is rising, but it has not built a trusted alternative. Europe is strategically lost. The rest of the world is diversifying, hedging, and recalibrating. This is the Thucydides problem expressed through currencies, bonds, and gold. The incumbent is no longer trusted enough to dominate unquestioned. The challenger is not yet trusted enough to replace it. The result is not a clean handover. It is contradictory pricing. In the old stable state, the dollar was the reserve asset, Treasuries were the safe asset, and gold was the hedge. In the next stable state, the dollar may remain important, but not supreme. Treasuries may retain nominal value, but lose real reserve privilege. Gold may become a core neutral asset on sovereign balance sheets. The world may move toward a multi-currency system built around dollars, gold, commodities, regional currencies, and bilateral settlement. The market is not confused. It is changing state. We are in the slush phase of the global monetary order. The old system still trades. The new system is already being priced. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

India’s Market Is Warning About Lower Growth : Vikas Sehgal

India’s Market Is Warning About Lower Growth The market is pricing a tougher future. Policy must deliver a stronger one. By Vikas Sehgal At current levels, India’s stock market is no longer pricing a cheap growth story. It is pricing a more difficult reality: India may be at risk of becoming a lower-growth economy. The market is not saying India will grow at 7–8% real GDP forever. It appears to be pricing something closer to a 5–6% real growth economy — still respectable, but no longer exceptional enough to justify complacency. That is the warning. Note: China adjusted = mainland China + Hong Kong market cap, to capture Chinese companies listed outside the mainland. India cannot afford to let its growth premium erode. If the government wants to protect that premium, it has to loosen the constraints on growth. That means reducing fiscal wastage, improving the quality of public spending, accelerating infrastructure execution, lowering friction for private investment, easing the burden on businesses, and allowing more capital to flow into productive sectors. India does not need more headline spending. It needs better spending. The risk is that too much fiscal capacity is absorbed by subsidies, bureaucracy, leakage, and low-return expenditure, while too little goes into productivity, logistics, manufacturing depth, energy security, and private-sector confidence. If that continues, India’s growth ceiling will fall. And the market is already beginning to price that risk. The market is giving India a warning, not a guarantee. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

Finish What You Start : Vikas Sehgal , Nishant Jain

Finish What You Start — The American Dilemma Understanding the problem and acting on it are two different things. By Vikas Sehgal, Nishant Jain Some of the sharpest strategic insights I’ve heard have not come from boardrooms or books — but over good food, from a man whose life has been anything but stable. A good friend of mine from Mathura — someone I admire deeply — Mr. D, has lived through more upheaval than most, and I’ve noticed that his clearest thinking tends to surface in the most unassuming settings. One such afternoon, over lunch at a small South Indian restaurant in Borivali, in North Mumbai, he delivered a long, almost theatrical explanation of his high blood sugar — what he couldn’t eat, what he shouldn’t eat, what the doctor had forbidden, what discipline demanded. It was precise, clinical, and entirely convincing. And then, without pause, he ordered dessert. Not something symbolic, but a full, unapologetic indulgence. I looked at him, amused. He smiled. “Understanding the problem and acting on it are two different things.” Then his tone shifted, and the conversation moved from sugar to something far more consequential. He spoke of the Brahmins of Mathura who chose defiance when faced with Mughal force, fully aware of the cost, because once the moment arrived, the choice was no longer theoretical — it was existential. And then of Hindu kings who, at decisive moments, chose restraint when force was required — not out of weakness, but out of misplaced virtue. “They were not wrong in values,” he said quietly. “They were wrong in timing.” That distinction reveals something modern states still struggle to accept: power is not persuasion; power is imposition. Once invoked — especially military power — the logic becomes brutally simple: you must win, and you must win decisively. Not because brutality is desirable, but because incomplete force is more destructive than decisive force. A war half-fought is not a restrained war — it is a war paid for twice. Before force is used, everything is open to debate — morality, legality, proportionality, long-term consequences. That is where contemplation belongs. But once the first strike is made, the nature of the problem changes. You don’t get to revisit the decision in parts or calibrate resolve in installments. You don’t get two decisions in war. The question is no longer whether to act; it becomes whether you are willing to finish what you have already started. History is unforgiving on this point. Hannibal Barca, after Cannae, had Rome exposed in a way few armies ever have. This was not a moment for brilliance; it was a moment for completion. Yet back home, caution emerged dressed as prudence. Arguments for restraint, for calibration, for limiting exposure began to dominate. Support slowed, commitment fragmented. It did not look reckless; it looked responsible. But every system produces this instinct — voices that appear measured and morally grounded, yet at the point of execution fracture resolve just enough to change the outcome. In war, that fracture is fatal. The enemy is given time, and time is the only resource a wounded system needs to recover. Rome did exactly that. It adapted, reorganised, and ultimately destroyed Carthage — not because it was stronger at the beginning, but because it was more decisive at the end. History does not reward restraint in the middle of execution — it punishes it. Hanno was not irrational. He represented a familiar instinct within political systems — the desire to limit exposure, to question escalation, to avoid overcommitment to a single path. His arguments would have sounded responsible, even principled. And that is precisely why they were effective. Every system produces its version of Hanno — figures who, at the moment of execution, fragment resolve in the name of prudence. They rarely see themselves as obstructing victory; they see themselves as preventing excess. But in war, that distinction collapses. Because hesitation at the point of advantage does not moderate outcomes — it alters them. The names change. The instinct does not. The pattern repeats. Prithviraj Chauhan defeated Muhammad Ghori in the First Battle of Tarain and had both advantage and initiative. What followed was restraint where resolution was required. Within a year, the outcome reversed, and with it, the trajectory of the subcontinent. Even advanced political systems fall into the same trap. Athens, during the Peloponnesian War, allowed internal pressures to override external necessity and recalled Alcibiades mid-campaign. The war did not pause; only Athens’ coherence did. The result was not moral credibility but strategic erosion. Once force is engaged, politics does not disappear — but if politics begins to dictate hesitation, the outcome is rarely stability. It is failure, only deferred. Because adversaries do not interpret partial force as restraint; they interpret it as hesitation, and hesitation is not neutral — it is an invitation. The most dangerous moment in conflict is not escalation — it is the illusion that one can pause without consequence. That was Mr. D’s real point. “Contemplation is a luxury before war,” he said. “Indulgence during it.” This is not a comfortable argument to make, and it is not one that many would have supported at the outset. I may be wrong on the specifics of this conflict. But the pattern itself is not new — and it is rarely forgiving. A decisive outcome will not be clean. It will involve loss of life, destruction, and consequences that cannot be reversed. There will be images that are difficult to justify and decisions that will be criticised for decades. The United States may well be wrong in how it arrived at confrontation with Iran — strategically, politically, even morally. The objectives may have been unclear, the escalation poorly framed, the endgame undefined. Those criticisms are valid, but they are no longer decisive. Because the moment force is used, the nature of the decision changes. This is not an argument for war. War is destruction, loss, and irreversible cost. It should always be

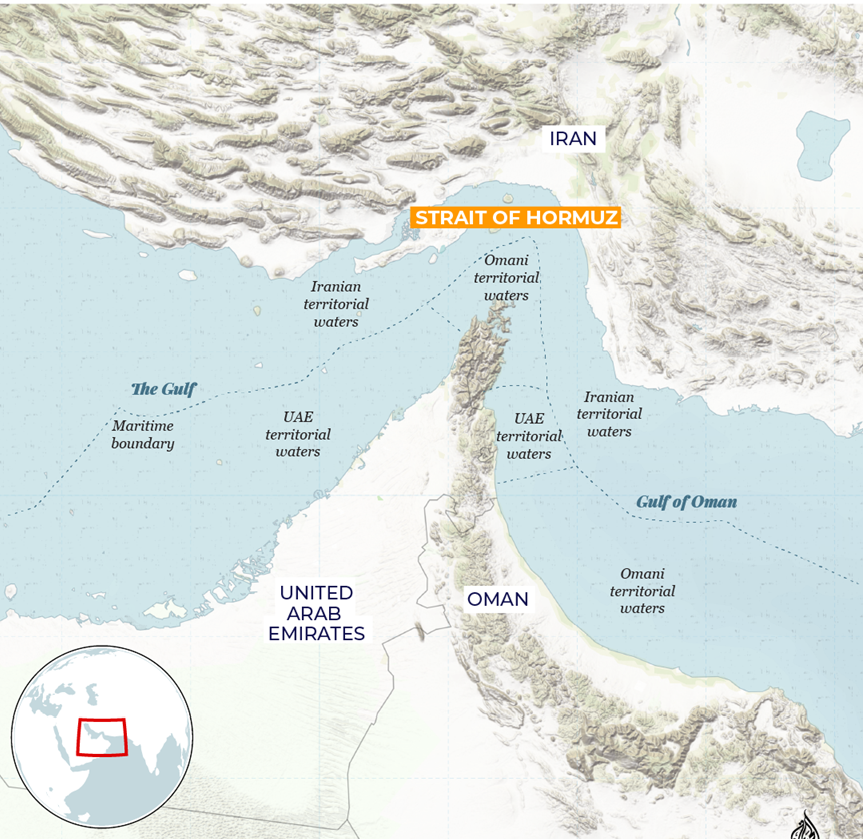

Gulf on the Edge : Vikas Sehgal, Saurav Agarwal

Gulf on the Edge: Why UAE Will Survive While Others Falter Gulf on the Edge: Why UAE Will Survive While Others Falter The Persian Gulf sits at the centre of global energy, finance, and geopolitics. Its oil powers economies across Asia, Europe, and the United States. Its sovereign wealth funds anchor financial markets. Its strategic location underpins US and allied military strategy. Yet beneath the gleaming skylines and enormous wealth lies a sobering reality: not all Gulf states are equally prepared for crisis. The UAE stands apart as resilient, diversified, and forward-looking. Bahrain, Qatar, and Kuwait, by contrast, face structural vulnerabilities that could trigger economic and social turmoil. Hormuz: The Strait that rules their fate The Strait of Hormuz is a chokepoint that defines Gulf vulnerability. Roughly 20% of global oil passes through this narrow passage. If exports are blocked, essential imports—particularly food—cannot arrive. The irony is stark: the Gulf, rich in hydrocarbons, is heavily import-dependent for basic goods. Iran, by contrast, is largely self-sufficient. Its energy, agricultural base, and domestic production allow it to endure shocks that would devastate smaller Gulf states. Rapid population growth, urbanization, and water scarcity in Bahrain, Qatar, and Kuwait magnify the impact of any disruption. Even a temporary blockade could create shortages and social unrest within weeks. The UAE, with advanced logistics, diversified import sources, and substantial reserves, is better positioned to manage such disruptions. Its infrastructure and strategic foresight provide a buffer that its neighbours lack. Economic Fragility: Wealth Is Not Immunity History shows that even small financial shocks can trigger massive systemic collapse. In the 2008 US mortgage crisis, less than 2% of homeowners defaulted, yet it nearly brought the global economy to its knees. The Gulf is even more sensitive. Its wealth, real estate markets, and sovereign funds rely on continuous confidence and capital mobility. If just 5% of expatriates or investors lose trust, it could trigger cascading failures: real estate prices collapse, capital leaves, and local banks face liquidity crises. The UAE’s sovereign reserves ($100B), diversified investments, and conservative fiscal policies give it a cushion. Smaller states—Bahrain ($36B), Qatar ($335B but highly concentrated), and Kuwait ($750B but with high per-capita expectations)—are far more exposed to even minor shocks. Dollar Pegs, Treasuries, and Global Interdependence The Gulf’s currencies are pegged to the US dollar, supported by massive investments in US Treasuries. But global forces strain this system: • China and India already hold substantial US debt, limiting Gulf purchases. • Europe faces its own fiscal deficits. • Korea and other defence-dependent states must redirect capital elsewhere, selling treasuries. If Gulf states cannot continue buying Treasuries, only leveraged hedge funds remain to absorb debt—a form of modern money printing. The result: potential dollar weakness, making currency pegs unsustainable. UAE’s diversified reserves give it flexibility to manage these pressures, but smaller states lack this buffer. US Policy: Rational for America, Risky for Allies The United States cannot indefinitely act as global reserve currency issuer while running massive deficits and deindustrializing its economy. Domestic priorities are shifting. For Gulf states, this creates a dilemma: the reliability of US naval protection, energy transit, and the petro-dollar system is no longer guaranteed. UAE’s prudent investments and independent planning reduce its exposure. Smaller emirates, heavily dependent on US guarantees, face an acute risk if Washington cannot maintain its presence. Historical Lessons: Allies Suffer When Powers Decline History offers cautionary examples of dependent states suffering when dominant powers falter: Rome: Economic and military decline led to abandonment of Britain and distant provinces, creating centuries of instability. Alexander’s Empire: Greek settlements in Central Asia were left marooned after his death, quickly losing political and economic viability. Hellenistic Cities of Asia Minor: Reliant on Greek support, they declined rapidly as central authority weakened. Mughal India: Regional vassals collapsed or realigned when the central economic base weakened. The lesson is clear: dependency magnifies vulnerability. For the Gulf, reliance on US protection, global finance, and energy markets means smaller states are highly exposed to systemic shocks. Why the UAE Stands Out Among Gulf states, the UAE’s approach is markedly different: Diversified economy: Energy contributes a smaller share of GDP than in neighboring emirates. Sovereign reserves: Significant assets provide a buffer against economic shocks. Strategic planning: Investments in logistics, tech, and alternative energy reduce dependence on single points of failure. Resilient institutions: Governance, rule of law, and regulatory frameworks instill confidence in investors. These factors make the UAE far more capable of surviving energy chokepoints, dollar volatility, or regional conflicts. Dark Prospects for Smaller Emirates Bahrain, Qatar, and Kuwait face multiple vulnerabilities: • High dependence on oil revenue and single-sector wealth • Smaller fiscal reserves relative to population and liabilities • Heavy reliance on expatriate labor, making even minor capital flight critical • Exposure to US protection and global financial flows Even minor disruptions—5% exodus of professionals, a temporary Hormuz blockade, or treasury market instability—could trigger cascading crises affecting real estate, sovereign wealth, and social stability. Entering an Uncharted Era The Gulf’s current stability masks underlying fragility. Strategic chokepoints, demographic pressures, financial interdependence, and reliance on external powers create a perfect storm. The UAE’s foresight and resilience position it to survive and adapt. Smaller emirates may not be so lucky. As global powers recalibrate, domestic priorities shift, and geopolitical tensions rise, the Gulf’s structural vulnerabilities are no longer theoretical—they are imminent and systemic. The UAE will likely weather the storm. Its neighbors face an uncertain, potentially dark future. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their

When Governments Run Out of Money : Vikas Sehgal, Saurav Agarwal

When Governments Run Out of Money… They Come for Your Gold. When Governments Run Out of Money… They Come for Your Gold. Every financial crisis eventually becomes a political one. At first, the problem appears technical — deficits, borrowing, monetary policy, temporary instability. Governments reassure the public that reforms are coming. Committees are formed. Experts debate solutions. But when the treasury finally empties and the options narrow, the problem becomes brutally simple. The state must find money. At that moment, the definition of wealth quietly changes. What citizens once called private property becomes, in the eyes of the state, available resources. History shows how this story ends. Not with polite defaults or careful restructuring. But with the sudden realization — often arriving at the end of a dusty road — that the state has decided it knows exactly where the wealth is. The Roman Republic learned this lesson many times. A Roman Senator and the Praetorian Guard A Roman senator sits on the shaded portico of his villa in Campania. The afternoon air is warm. A Greek slave reads Homer — the fall of Troy, a city that believed its walls eternal. The senator listens half-heartedly. His thoughts drift to accounts and estates: grain from Sicily, rents from vineyards in Gaul, and the gold he accumulated during his years as governor of Upper Gaul. Then he sees it. A cloud of dust rising on the distant road. Hoofbeats follow. Praetorian cavalry. He does not need to ask why they have come. The emperor — perhaps Tiberius, perhaps another — has declared him an enemy of the state. The charges will be vague: corruption, disloyalty, treason against Rome. But the senator knows the real reason. The treasury is empty. They are not coming for his slave. They are not coming for his harvest. They are coming for his gold. What will follow will be described as justice. As necessity. As fairness in service of the Republic. But it is confiscation. Pure and simple. And it has happened before. And it will happen again. The Oldest Pattern in Politics When states run out of money, they follow a path as old as civilization itself. The sequence rarely changes: Deficits → Currency Debasement → Capital Controls → Confiscation It does not matter whether the system is a monarchy, a democracy, or a revolutionary regime. The motive is the same everywhere. Power must be preserved. Politicians who spend win elections. Rulers who distribute wealth secure loyalty. Debt postpones consequences. Eventually, the bill arrives, and the state begins searching for assets. By now the pattern should be obvious. History shows where it looks first. Stage One — The Appetite of the Empty Treasury Empires rarely collapse because of invasion first. They collapse because of promises they cannot afford. Athens offered one of the earliest warnings. In the 5th century BC, Pericles moved the treasury of the Delian League from Delos to Athens. Funds meant for collective defence quietly became funding for monuments — the Parthenon, temples, and civic works glorifying the city. The money belonged to the alliance. But Athens spent it anyway. Rome repeated the pattern centuries later. Civil wars drained the treasury. Armies demanded pay. Politicians promised land and rewards to veterans. When money ran out, Rome found another solution. Proscriptions. In 82 BC, Sulla published lists of wealthy citizens in the Forum. Anyone named could be killed without trial. Their property was confiscated by the state. Heads of the condemned were sometimes displayed in the Forum — a grim reminder that the lists were not theoretical. Gold flowed into the treasury. A generation later, the Second Triumvirate — Mark Antony, Octavian, and Lepidus — revived the practice. Thousands died. Estates were seized. Even Cicero Rome’s greatest orator, was hunted down and executed. Armies were paid. Power was secured. Stage Two — The Vanishing Coin When confiscation cannot keep pace with spending, rulers turn to the currency itself. Rome provides the textbook case. In the early empire, the silver denarius contained nearly pure silver. By the third century AD, emperors desperate to fund armies and bureaucracies began diluting it. Silver content collapsed. The coin looked the same. Its value did not. Prices surged. Trade faltered. Confidence vanished. Diocletian imposed price controls. Constantine introduced new coinage. But the underlying problem remained. The state was spending far more than it could fund. Modern governments rarely debase coins with copper. They achieve the same effect through monetary expansion, inflation, and debt monetization. Savings lose value. Capital begins searching for refuge. And throughout history, that refuge has often been gold. Stage Three — The Locked Vault When capital begins fleeing a failing monetary system, governments respond predictably. They close the exits. China provides early examples. The reformer Wang Mang attempted sweeping nationalizations of land and wealth during the first century AD. Centuries later, the Qing emperor Yongzheng confiscated fortunes of officials accused of corruption. Modern history offers equally stark examples. In 1968, India passed the Gold Control Act, restricting private ownership of bullion and forcing citizens to convert holdings into jewelry or surrender them to the financial system. In 2013, Cyprus delivered a shock. Depositors woke to discover their bank accounts frozen. Withdrawals were restricted. A portion of deposits was simply seized to recapitalize failing banks. The message was unmistakable: wealth inside the system can be trapped overnight. Stage Four — The Final Claim Eventually the state turns toward the asset citizens believed would protect them from monetary collapse. Gold. History offers relentless examples. During the French Revolution, the government seized church lands and precious metals to support the collapsing assignat currency. In 1933, the United States ordered citizens to surrender their gold. Private ownership was banned; citizens were forced to sell at $20.67 per ounce. Shortly afterward, the government raised the price to $35. The difference went to the state. In India, gold ownership was restricted for decades. In Cyprus, deposits became the target. The pattern is clear: gold is treated as insurance by citizens,

The China Imperative India’s Race Against Time : Vikas Sehgal, Saurav Agarwal

The China Imperative Indias Race Against Time The China Imperative Indias Race Against Time Why factories, not handouts, will decide India’s future. While India promises ₹15,000 crore in welfare handouts, China quietly builds 500 factories per month. One country is spending on votes. The other is building power. The gap is widening—and it is not just about money. It is about factories, technology, energy security, and industrial depth. Every year India delays industrial investment, China adds more factories, more research labs, and more supply chains that the world will rely on for decades. This is not a drill. Political handouts may win elections. But factories win wars, build independence, and secure futures. India’s race is not just economic—it is existential. And time is already running out. Factories, Not Votes India’s industrial base remains shallow. Manufacturing contributes roughly 15–17% of GDP, compared with 30–35% in China. Research and development is similarly lagging: India spends 0.8–1% of GDP, China 2–2.5% (note: of a base that’s 5x that of India) Energy infrastructure is unreliable. Logistics remain fragmented. Ports, rail networks, and power grids are far behind global standards. The result: India cannot scale production in critical sectors like electronics, electric vehicles, shipbuilding, or industrial machinery. Meanwhile, China builds the factories that supply the entire world. Every year India dithers, China compounds its advantage. This is the arithmetic of power. Factories, supply chains, and energy security do not wait for elections. The Cost of Welfare Politics Meanwhile, electoral politics reward short-term spending. Cash transfers, subsidies, and schemes like Ladli Behna multiply across states. The annual cost of these programs runs into tens of thousands of crores, often funded by borrowing. Borrowing for consumption is easy. Borrowing for capital is hard. But it is the hard choices that determine national destiny. Every rupee spent on welfare programs is a rupee not invested in a factory, a research lab, or an industrial corridor. India’s fiscal numbers tell a worrying story: combined central and state debt is now 85–90% of GDP, with interest payments consuming over 23% of government revenues—more than defense spending. This is debt funding short-term happiness, while long-term power erodes silently. Geopolitics Is Unforgiving India shares a long and contested frontier with China, whose economy is roughly $20+ trillion—nearly five times India’s $4+trillion. China produces three times more manufactured goods, spends four times as much on R&D, and dominates high-tech industrial sectors from electronics to EVs to shipbuilding. Economic scale is not abstract. It translates directly into military capability, technological dominance, and strategic leverage. Dominant powers rarely tolerate rising neighbors unchecked. Every month India delays industrialization, China widens the gap. Historical benchmarks suggest that for India to remain strategically autonomous, it must eventually reach 40–60% of China’s GDP. Today, India sits closer to 20%. Below that threshold, sovereignty becomes increasingly theoretical. At best, India risks becoming a quasi-vassal—formally independent, but structurally constrained. Lessons from History History is merciless. The Ming Dynasty in China collapsed when fiscal mismanagement and subsidies undermined industrial and military capacity. Short-term generosity calmed the population but hollowed out power. Within decades, the dynasty fell, replaced by the Qing. Modern parallels abound. Argentina squandered its prosperity on consumption and subsidies; Sri Lanka collapsed under the weight of debt-funded populism. The lesson is simple: nations that prioritize capital survive. Nations that prioritize handouts drift into dependency. The Urgency Is Now Consumption does not build power. Capital does. Factories matter. Technology matters. Energy matters. Supply chains matter. Rhetoric does not build nations. Balance sheets do. India still has a narrow window. Build factories now. Invest in technology now. Accumulate national capital now. Because the arithmetic of power compounds as relentlessly as the arithmetic of debt. Political incentives push in the opposite direction. Every election expands giveaways. Every subsidy becomes permanent. Every promise must be outbid by the next politician. This is how fiscal systems drift toward collapse. Economics does not care about slogans. Mathematics does not respond to compassion narratives. Debt compounds quietly—until suddenly it doesn’t. Nations rarely collapse overnight. They drift there slowly. And then one day, the world notices. By then, the arithmetic is irreversible. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

What Can Warsh Do ? : Vikas Sehgal, Saurav Agarwal

What Can Warsh Do ? What Can Warsh Do ? Let’s skip the complex math, the sacred economic texts, and the chanting about repo facilities. This is basic arithmetic. It doesn’t care who the Fed Chair is. The U.S. economy is roughly a $30 trillion machine carrying about $38 trillion in debt. That debt grows by close to $2 trillion every year, automatically. Interest payments are now approaching $1 trillion annually and compounding at 15–20 percent a year. That’s impressive growth—just not the kind anyone should be celebrating. At this point, asking what Kevin Warsh will do is like asking which button the elevator will press after the cables have snapped. The math problem is painfully simple. The U.S. government spends about $7 trillion a year and collects roughly $5 trillion in taxes. This isn’t politics; it’s subtraction. The idea of “paying down the debt” belongs in the same museum as the gold standard and balanced budgets. To merely stop the debt-to-GDP ratio from getting worse, the United States would need around 8 percent nominal GDP growth every year. For an economy of this size and complexity, that implies something like 5 percent inflation and 2 to 3 percent real growth—and that’s on a good day. To actually reduce the debt burden, the numbers get uglier. You need double-digit nominal growth, which means inflation north of 7 percent alongside positive real growth. At that point, the Fed’s 2 percent inflation target stops being a policy goal and becomes an aspiration. So what will Warsh do? Here’s the uncomfortable truth: Warsh doesn’t decide. Arithmetic does. He’s just the narrator, and there are only two possible stories to tell. In the first story, the Fed fights inflation. Rates rise, inflation comes down, and economists applaud. Then reality intrudes. Interest costs explode, economic growth slows, markets fall, and tax revenues collapse—income taxes, capital gains, stock options, all evaporate. The deficit widens far beyond today’s already grotesque $2 trillion annual increase. Bond yields spike. The dollar wobbles. At that point, the Fed faces a binary choice: print money or default. Default is politically impossible. Printing is patriotic. The dollar dies. In the second story, the Fed fights the debt. Rates come down and inflation takes off. Eggs begin to cost more than gasoline. Wages chase prices. Voters scream. But inflation at 7 to 8 percent performs the only remaining trick in the playbook: nominal GDP surges into double digits, and the debt suddenly looks manageable—at least on paper. Meanwhile, the dollar quietly slips out the back door. And dies. Two paths. Same ending. So no, the real question isn’t what Warsh wants to do. The real question is whether the dollar dies by high interest rates or by inflation. This isn’t policy; it’s choreography. The outcome is already locked in. The only suspense left is how loudly everyone pretends to be surprised. Which brings us to India—and to you. Warsh’s fate is sealed. India’s, and yours, is not. There’s no point debating what the RBI or policymakers should have done when the freight train was still in the distance. You should have heard it coming. Now you can see it, and it’s close. So let’s talk about tomorrow. The survival formula is brutally simple: run, and run fast. Strengthen your balance sheet as quickly as possible. Own assets that effectively short the dollar—the larger your exposure, the better. Watch what China is doing as it buys an extra million barrels of oil a day for its strategic reserves. You may not have storage tanks, but you can position yourself in commodities or equities that benefit from a weakening dollar. The bottom line is unavoidable. Dollar decline is inevitable. The only question is how fast it happens—and whether you get out in front of it. Act accordingly. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

The Age of Fiscal Illusion : Vikas Sehgal, Saurav Agarwal

The Age of Fiscal Illusion The Age of Fiscal Illusion When Democracies Run Out of Your Money “Empires rarely collapse because of a single catastrophe. They collapse because the math finally catches up with the politics.” “Democracy is the worst form of government—except for all the others that have been tried.” The observation by Winston Churchill has endured because it captures a fundamental truth. Democracy is inefficient, chaotic, and often irrational. Yet compared with monarchy, dictatorship, or technocracy, it has proven remarkably resilient. But the democracy Churchill defended is not the democracy that exists today. Over the past century, something fundamental has shifted. The relationship between citizens, the state, and economic responsibility has been quietly rewritten. What began as a system grounded in shared obligation has gradually evolved into something else entirely: a political machine capable of redistributing wealth on an immense scale. For decades, the system seemed stable. Now it is colliding with arithmetic. Across much of the world, governments are confronting a problem they can barely admit aloud: they are running out of money that belongs to other people. And history suggests that when states reach this point, the consequences are rarely mild. The Forgotten Contract The earliest democratic systems were built on a simple premise: power required responsibility. In the city-states of ancient Greece, political participation was largely restricted to male citizens who owned property and served in the military. Citizenship was not merely a privilege—it was a burden. The same logic governed the Roman Republic. Property ownership determined political influence, and political influence carried military obligation. Citizens voted for wars—and then fought them. They approved taxation—and then paid it. Political decision-making and economic responsibility were inseparable. Modern democracy gradually dissolved that link. Industrialization, social reform, and the moral force of equality expanded suffrage until nearly every adult gained the right to vote. The transformation was morally compelling and politically inevitable. But it also altered the internal incentives of the system. The ballot box ceased to be merely a mechanism of representation. It became a mechanism of allocation. “Once voters realize the treasury can be accessed through elections, politics becomes a competition to divide the spoils.” Democracy as Distribution In theory, redistributive policies can strengthen societies. Modern welfare states emerged after the devastation of the Second World War and played an important role in stabilizing economies and reducing poverty. But democratic systems operate under powerful incentives. Politicians must win elections. Winning elections requires assembling coalitions. Coalitions are often built through promises. Subsidies. Transfers. Tax credits. Public employment. Industrial policy. Each policy may be defensible on its own. But over time the promises accumulate. And eventually the promises exceed the resources available to fund them. Political rhetoric frequently centers on the idea of “taxing the rich.” It is a potent slogan. But as a long-term fiscal strategy, it rarely works. Capital in the modern world is extraordinarily mobile. Wealthy individuals can shift assets, restructure holdings, or relocate across borders with relative ease. Capital travels lightly. The middle class does not. In practice, the financial backbone of the modern state becomes the salaried professional, the small business owner, and the middle-income household tied to a job and a location. Meanwhile, the political class itself often prospers. Across many democracies, those who enter politics emerge far wealthier than when they began. Public service is theoretically about sacrifice. In reality, there is often no business quite like the business of the state. The Limits of Taxation Eventually, even the most ambitious redistributive systems encounter limits. Economists describe one such limit through the Laffer Curve. At low tax rates, raising taxes increases government revenue. But beyond a certain threshold, higher taxes begin to discourage work, investment, and entrepreneurship. Push the tax burden too far and revenues begin to fall. Many advanced economies are already approaching that boundary. In large parts of Europe and North America, total tax burdens approach or exceed 40–50 percent of GDP. Beyond that level, further increases risk suffocating the economic engine that produces tax revenue in the first place. But democratic systems rarely shrink gracefully. When taxation reaches its limit, governments turn to borrowing. “Debt allows democracies to postpone reality. It does not eliminate it.” The Seduction of Debt Borrowing is politically irresistible. It allows governments to deliver benefits today while shifting the cost into the future. Current voters receive services. Future taxpayers receive the bill. For decades this arrangement appeared sustainable. Interest rates remained low, global savings were abundant, and financial markets willingly absorbed enormous quantities of government debt. But debt compounds. Eventually, interest payments begin consuming large portions of government budgets. Fiscal flexibility disappears. Many major economies have already crossed the threshold where government debt approaches—or exceeds—the size of the national economy. At that point the political choices become brutally constrained. Raise taxes and risk economic contraction. Cut spending and face electoral revolt. Or reach for the oldest fiscal trick in history. Debase the currency. The Ancient Art of Debasement Currency debasement is as old as government itself. In the ancient world, rulers shaved precious metals from coins. In the modern world, governments expand the money supply. The mechanics differ. The outcome is the same. Reduce the value of money, and the real burden of debt declines. As the economist Milton Friedman famously observed, governments have only three ways to finance spending: taxation, borrowing, and inflation. Inflation is taxation carried out quietly. It reduces the purchasing power of wages. It erodes savings. It redistributes wealth from the prudent to the leveraged. For governments trapped by rising debt and political resistance to austerity, inflation is often the path of least resistance. History suggests it is also the path of greatest danger. “When states cannot tax more and cannot borrow more, they print.” Rome: When Money Stops Meaning Anything The late Roman Empire provides a chilling example. During the third century, the empire faced spiraling military costs and political chaos. To finance the state, successive emperors debased the silver denarius. Over time, the coin’s silver content collapsed. Prices surged. Trade deteriorated. Tax collection became increasingly difficult.

AI Goes Deeper Than You Think: Vikas Sehgal, Vinayak Khedekar

AI Goes Deeper Than You Think AI Goes Deeper Than You Think And Rome Already Told the Story The real risk of AI is not unemployment. It is irrelevance. Most people think AI is about jobs. It isn’t. This essay is an attempt to assess the societal impact of artificial intelligence. Rather than beginning with technology, it looks to history—specifically for moments when the supply of labour shifted suddenly and structurally, rather than gradually. One such episode follows the Punic Wars, when Rome experienced a rapid infusion of slave labour—effectively near-zero-cost, abundant, and scalable—which disrupted an agrarian economy built on human effort. In studying how this shift altered economic structures, social order, and political outcomes, this essay seeks to outline not a prediction, but a plausible direction. AI may be unprecedented in form, but not entirely in consequence—and its closest parallel may lie in what such a shock could mean for modern knowledge economies, from Rome then to Bangalore now. To understand the future, the past is not a guide—it is a warning. The morning begins in mist. You stand on a low ridge in Tuscany. The soil is dark, soft, alive. The air carries olives and wet earth. Light moves slowly across vines, grain, stone. This is your land. You—Antonius, a small farmer—work it with your sons, while your wife measures everything without scales: grain, oil, time. Nothing is abundant. Nothing is wasted. Effort becomes income, and income becomes survival. The system holds because the wage holds—even when paid in crops rather than coin. Across a low stone boundary sits another world. The senator’s estate stretches further than you can see. Where your effort defines output, his ownership multiplies it. You notice the difference. It does not yet threaten you. You are a Roman citizen—equal in theory. That theory is about to expire. Then the news arrives. Victory in the Punic Wars. Rome celebrates. You are invited to the villa. Wine flows. Music plays. Then you see them—rows of able-bodied men, chained, silent. Not workers as you understand them, but controlled labour: labour that does not negotiate, does not leave, and does not require wages. You do not understand it yet, but the system has already changed. You will understand later—when reversal is no longer possible. Rome did not invent this moment. It revealed it. Slave labour floods the economy. Small farmers are displaced. Land consolidates. Citizens move into cities without work. Antonius is fictional. What happens to him is not. The next season looks the same. The arithmetic is not. The senator does not hire. His costs collapse. His grain reaches the market first—and cheaper than yours. You work longer. Your sons work harder. It does not matter. You are no longer competing against a better farmer. You are competing against labour priced outside wages. Within two seasons, the outcome is mechanical. You sell—not because you failed, but because the system stopped pricing what you do. Losing the land is not the real loss. You move to Rome. Rome absorbs you. It does not employ you. The streets are full—not of work, but of people. Farmers from across the Republic, displaced by the same force: capital combined with labour that costs nothing. Too many hands. Nothing for them to do. You wake later—not from rest, but from absence. There is nothing to wake up for. The rhythm of life breaks. Your older son stops asking about the farm. Your younger stops trying. The skills you built over a lifetime have no use—even inside your own home. This is not poverty. It is loss of function. The first time you stand in line for grain, you feel it—not hunger, but something deeper. The men around you do not work, yet all will eat. This is annona—grain distribution. Not charity, but control. A system built on a new reality: Rome no longer needs its citizens to produce, only to remain stable. Bread is distributed. Games are organised. Time is filled. Life is not. Then come the voices. The Gracchi brothers—Roman reformers arguing that wealth concentration has gone too far, that the system has detached from the citizen (early populists, inside the Senate). You listen. For the first time, someone names the problem. It is not you. It is the structure. You feel something you have not felt since leaving your land: recognition. They propose restoration—return land, rebuild the link between effort and survival. The Senate resists. Tiberius is killed. Gaius continues, expanding grain, formalising distribution. He too is removed. But the idea survives them. When wages fail, politics replaces them. Then comes Marius—a general who understands the new Rome. He recruits not landowners, but men like you: displaced, unnecessary, surplus (a shift from citizen-army to employer-army). You understand immediately. The Republic no longer needs you, but it will take your son. Your eldest leaves—not for glory, but for income, identity, and purpose. Rome expands. But something fundamental has already broken. Loyalty is no longer tied to land or Republic. It is tied to whoever provides. Rome is not the story. It is the template. What took decades then will take years now. Rome made labour cheap. AI makes labour irrelevant. Slaves required food, control, containment. AI requires power. Slaves could resist. AI cannot. Rome scaled through conquest. AI scales through code. Rome was local. This is global. The modern economy runs on cognition. Cities like London, New York, Bangalore, and Hyderabad convert intelligence into income. That layer is now being priced toward zero. You cannot compete with something that does not need to be paid. Markets will understand this before society does. Multiples compress first. Earnings lose scarcity. Equity reprices before jobs disappear. Employment follows. Then the state—because the modern state is funded by this layer. London is not a city. It is the UK’s tax base. As cognition loses value, the state weakens. Real estate follows income. Offices empty. Valuations fall. Real estate is not property. It is income, capitalised. Remove the income, and it reprices. Banking compresses

Bankrupting Itself: An Indian Story : Vikas Sehgal, Nishant Jain

Bankrupting Itself: An Indian Story Bankrupting Itself: An Indian Story How welfare politics are weakening India while China builds power. The most dangerous policies rarely look dangerous. They arrive wrapped in fairness, empathy, and moral virtue. Politicians have perfected the art of selling policies that are disastrous for the long-term health of the nation—while convincing voters they are acts of generosity. It is not unlike my daughter persuading me to hand over my credit card for a Black Friday spree: everyone feels good… until the bill comes. Human psychology makes this possible. We are wired to admire those who appear to stand for good. In prehistoric tribes, survival depended on appearing fair and aligned with the group. When a predator appeared outside the cave, the tribe had to act collectively. Being perceived as moral increased the odds that others would defend you. Today, modern politicians exploit the same instinct. In India, this instinct has a price. The country is still transitioning from a lower-middle-income stage and desperately needs capital investment—factories, energy, technology, infrastructure. Instead, electoral competition increasingly rewards short-term consumption. Cash transfers, subsidies, and welfare schemes like Ladli Behna multiply across states, costing tens of thousands of crores annually. Borrowing to fund this consumption is like giving sugar to a diabetic: it feels kind, but it accelerates the disease. Imagine a family drowning in debt. One son runs a profitable business. The other spends money. The father borrows more and gives it to the spender. The productive son stays silent to avoid appearing selfish. The spender is happy. The productive son’s silence becomes the family’s downfall. Modern welfare politics often mirrors this pattern. India’s combined central and state debt is nearing 85–90% of GDP. Interest payments alone now consume roughly 23–25% of government revenues—more than the national defense budget. Punjab’s debt exceeds 45% of state GDP. Kerala’s is around 38–40%. West Bengal’s debt is near 37–38%. Productive states such as Maharashtra, Gujarat, and Karnataka carry far lower debt burdens, but fiscal federalism effectively channels capital from the productive to the unproductive. Once welfare commitments appear, they rarely disappear. Each election forces politicians to promise more than the last. Lakhpati behna today. Crorepati behna tomorrow. The arithmetic of generosity compounds quietly—until suddenly it doesn’t. This dynamic is not unique to India. Argentina once ranked among the world’s ten richest economies. Decades of borrowing, populism, and currency debasement reduced it to repeated sovereign defaults. Sri Lanka followed a similar path, culminating in a full-blown fiscal crisis in 2022. History even provides a lesson from India’s neighbor. Late in the Ming Dynasty in China, the court faced mounting pressure to maintain subsidies, grain transfers, and regional appeasement while revenues stagnated. Short-term expedients kept the population calm, but military funding weakened and regional administrations hollowed out. Within decades, the dynasty collapsed, replaced by the Qing. Fiscal decay rarely looks dramatic when it begins—it usually looks compassionate. The Scottish philosopher Adam Ferguson observed that when interest payments exceed defense spending, fiscal foundations begin to crumble. The United States recently crossed that threshold. Less discussed is that India, combining central and state finances, is already uncomfortably close. And then there is geopolitics. India shares a long and contested frontier with China, whose economy is roughly $18 trillion—almost five times India’s $3.7 trillion. China produces three times more manufactured goods, spends over four times as much on R&D, and dominates critical industrial sectors from electronics to shipbuilding to EVs. Economic scale translates directly into military capability, technological edge, and geopolitical leverage. Dominant states rarely tolerate powerful neighbors rising unchecked. For India to remain a civilizational power with real autonomy, its economy must approach 40–60% of China’s size, based on historical benchmarks. Today India sits closer to 20%. Below this threshold, sovereignty becomes increasingly theoretical. At best, the smaller state becomes a quasi-vassal—formally independent, but structurally constrained. Consumption does not build power. Capital does. Factories matter. Technology matters. Industrial depth matters. Rhetoric does not build nations. Balance sheets do. And balance sheets are built through investment, discipline, and industrial ambition—not debt-funded generosity. India still has a narrow window. Build a deep industrial base now. Invest in technology now. Accumulate national capital now. Because the arithmetic of power compounds as relentlessly as the arithmetic of debt. But political incentives push in the opposite direction. Every election expands giveaways. Every subsidy becomes permanent. Every promise must be outbid by the next politician. This is how fiscal systems break. Economics does not care about compassion narratives. Mathematics does not respond to slogans. Debt compounds quietly—until suddenly it doesn’t. Nations rarely collapse overnight. They drift there slowly. And then one day, the bond market notices. By then, the arithmetic is already irreversible. Disclaimer This article is published for informational purposes only and does not constitute investment advice or analysis. The information presented has been sourced from public domains and has not been independently verified. Vasuki Group makes no representations or warranties regarding the accuracy, completeness, timeliness, or reliability of the content. Neither Vasuki Group nor its affiliates, directors, employees, or representatives shall be liable for any errors, omissions, or reliance on the information provided. This article does not constitute an offer, solicitation, or recommendation for any investment, securities transaction, or contractual engagement. Readers should conduct their own due diligence before making any financial decisions. Any views expressed are those of the author and do not necessarily reflect the opinions of Vasuki Group. Further, Vasuki Group may hold or take positions in the market that differ from the views expressed in this article. All rights reserved. Vasuki Group reserves the right to update or modify this article at its discretion. For more information, reach out to us on research@vasukiindia.com.

Temple & Treasury : Vikas Sehgal, Nishant Jain